Editor's Note: This is Redpoint VC's Tomasz Tunguz' second article in a series examining trends in the public and private technology markets.

Last week, we discussed four trends in the public technology markets. Today we compare the current state of the US venture capital to historical norms.

First, we will examine the inflows into the venture capital market: dollars raised by venture capitalists. Then we will explore the outflows, VCs' investment pace, contrasting the dollars deployed over time. Last, we will investigate market sentiment and consequent price fluctuations.

Venture Dollars Raised Fall 27% Below 15 Year Trailing Median

The venture capital industry is in the midst of a contraction. Since 2001, limited partners have invested a median of $22B each year in venture capital. Over the last 3 years, those figures have dropped by 50% to $16B annually.

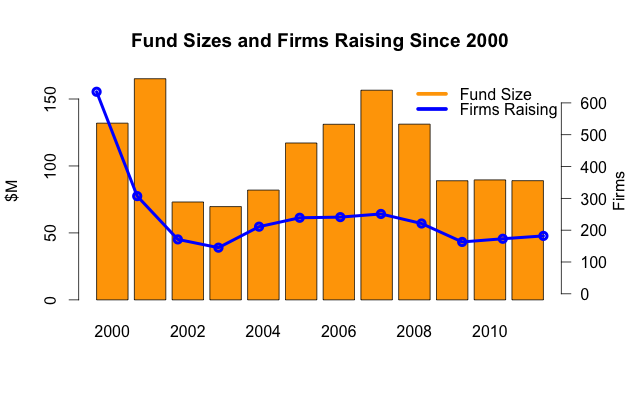

Venture Funds are 14% Smaller

There are fewer firms investing less money from smaller funds in 2011 than on average over the past 12 years. In 2011, 182 venture firms raised funds, about 16% below the 12 year median. The average 2011 venture fund is 14% smaller than the 12 year median.

However, there is increasing concentration of capital in well-known firms – a flight to quality phenomenon. Historically, the top 25 firms have raised about 30% of all venture dollars. During the first half of 2012, the top 10 firms raised 69% of all dollars, a tremendous concentration. These large funds skew average fund size upward suggesting smaller firms are disproportionately affected by decreasing fund sizes governed by a declining LP capital base.

Venture Investing Pace is Precisely Average

Despite the trends in the fundraising market, 2011 was an average year for venture investing. Over the last 12 years, venture capitalists have invested in 3076 US startups annually on average. In 2011, 3206 startups raised venture capital representing an insignficant 4% decline. Over the past 10 years, VCs have invested on average $33.8B annually and 2011 again matched the average at $32.6B. Both investment pace and investment dollars are on the rise, a seemingly positive signal.

Investing pace cannot remain constant forever because venture capital inflows are declining. But this rate may be maintained for a few years. VCs raise funds for ten years and typically invest all the dollars raised within the first four years. The difference between dollars raised and invested is called the overhang. This overhang provides the extra capital to maintain the current investment pace.

Investment Sizes Are Growing in Later Stages

Although most pricing data is private, we can use median investment size as a proxy for pre-money valuations if we assume the ownership stake a VC takes in an investment has remained constant over time.

Seed investment sizes have remained relatively constant over the past ten years, although the data is most sparse for this asset class since many investments are unreported. Series A prices have been declining steadily over the past 10 years at a rate of -5%, while Series B and Growth investments fell dramatically during the financial crisis. As public market prices fell, so did Series B and Growth valuations. However, these negative trends have reversed in the past year: Bs and Growth rounds have increased in size and are now both about 10% greater than the 12 year mean.

These data contradict the market perception of ever-larger rounds at ever-better prices.

A Tale of Two Markets

Performing analyses on the median investment sizes masks the outliers who make headlines and consequently are the most visible indicators of the state of the fundraising market.

Performing analyses on the median investment sizes masks the outliers who make headlines and consequently are the most visible indicators of the state of the fundraising market.

The average dollars invested across all stages has risen by 25% since 2008, implying outliers raise money at sufficiently high prices to dramatically skew the average higher than the median. Much like the venture capitalists who invest in these companies, a few very high profile startups are raising disproportionate amounts of capital. Over the past 12 years the difference between average and median investment sizes have never been as great as the past 2 years. In 2010 and 2011, the average investment is twice as large as the median investment.

These pricing trends describe a tale of two markets. A small number of brand name startups raise large, generously priced rounds from top investors with large funds skewing data upward. Meanwhile the rest of the venture capital market has contracted and investors are maintaining strong price discipline, investing in relatively smaller rounds at lower prices.

Reversion to the Mean

The venture capital market is evolving. It's reasonable to expect most of the metrics describing the venture capital industry to trend toward the mean: slight increases in dollars invested in venture capital, continuity for investment pace and capital deployed, steady valuations in early rounds but declining valuations in later rounds. Such a reversion make take time. After all, early 2012 data on the fundraising market indicates contracting trends are persisting. For now, at least, the market is in a Dickensian state.

NB: Data used in this analysis are publicly available through Dow Jones VentureSource and the NVCA

Featured image: Getty/Phil Ashley

No hay comentarios:

Publicar un comentario